Introduction

Brands are spending more than ever on advertising, yet the audiences they're trying to reach have never been more skeptical, more distracted, or better equipped to ignore them entirely. Consumer trust in advertising is under genuine pressure — and for media buyers, that's a commercial problem, not just a perception one.

The stakes are real. According to the Advertising Association's Credos research, trust has leapt from seventh to second place as a driver of brand effectiveness and financial performance over the past decade. That shift reframes trust from a soft brand metric into a hard commercial variable.

But trust isn't uniform. It varies dramatically by region, generation, and channel — and the gap between high-trust and low-trust markets is widening. Understanding where trust is strong, where it's eroding, and why it's collapsing in specific channels is now essential for anyone making media investment decisions.

Key Takeaways

- Word-of-mouth remains the most trusted advertising format globally — 88% of consumers trust recommendations from people they know

- Regional trust gaps are significant: Latin America, MENA, and Asia-Pacific consumers trust advertising more than those in North America and Europe

- Millennials and Gen X trust advertising more than Gen Z and those over 55

- TV, print, and newsletters consistently outrank digital and social formats in consumer trust

- Trust is now measurably linked to brand profitability, making it a core input for media planning decisions

The Global Trust Deficit: Where Things Stand Today

What "Trust in Advertising" Actually Means

Trust in advertising refers to the degree to which consumers believe an ad is honest, credible, and worth acting on. Liking an ad is not enough — the real measure is whether a consumer lets it influence their decisions.

Measuring this globally has become a strategic necessity. Nielsen's 2021 Trust in Advertising Study surveyed 40,000+ consumers across 56 countries, one of the most cited public datasets on the topic. Its headline finding: trust is substantially stronger in Africa, the Middle East, and Latin America than in North America and Europe — though exact regional percentages require access to the full paid dataset.

The Trust-Action Connection

Low trust doesn't just mean passive indifference. It produces active avoidance. Consumers who distrust advertising:

- Use ad blockers — eMarketer reports 32.8% of worldwide internet users use ad blockers at least sometimes

- Skip, mute, or scroll past ads reflexively

- Develop negative associations with brands that appear in low-trust contexts

Meanwhile, UK public trust in advertising hit 40% in 2025 — its highest in five years, up from 31% in 2021, per the Advertising Association's Trust Tracker. Progress is happening, but slowly.

What Drives Trust and Distrust

Credos research is unusually specific here. Enjoyment is the single biggest factor in determining whether someone trusts an ad. The inverse is equally clear: bombardment — being overwhelmed by volume — is the single biggest driver of distrust.

Credos's trust driver analysis puts hard numbers to both forces:

- Enjoyment/creativity scores 31 out of 100 as a trust driver

- Bombardment rose from 19 to 32 out of 100 among younger audiences in a single year

That near-doubling of the bombardment score in one year is a direct signal for brands: ad frequency decisions are no longer just a media planning detail — they're a brand trust variable.

Key Trends Reshaping Trust in Advertising Globally

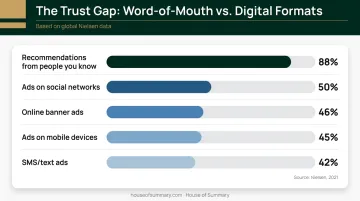

Trend 1: Word-of-Mouth Reigns — and Digital Falls Short

Nielsen's 2021 Trust in Advertising Study puts peer recommendations at 88% trust globally — the highest of any format measured. No paid channel comes close.

The gap between word-of-mouth and digital formats is striking:

| Format | Trust Level (US, 2021) |

|---|---|

| Recommendations from people you know | 88% (global) |

| Ads on social networks | 50% |

| Online banner ads | 46% |

| Ads on mobile devices | 45% |

| SMS/text ads | 42% |

Every dollar invested in customer experience, referral programs, and review generation is, effectively, investment in the highest-trust advertising channel available.

Trend 2: Influencer Advertising Is More Complex Than It Looks

Nielsen's data presents a nuanced picture. A 2022 Nielsen article citing the 2021 study found that 71% of consumers trust advertising, opinions, and product placements from influencers — a higher figure than is often cited in coverage of influencer skepticism.

What the data doesn't fully capture is variation within influencer marketing:

- Celebrity one-off posts attract more skepticism and regulatory scrutiny (the ASA's 2024 influencer disclosure report found persistent non-compliance on Instagram and TikTok)

- Micro-influencers with smaller, niche audiences tend to generate stronger perceived authenticity

- Long-term brand partnerships outperform transactional sponsored posts in sustaining trust over time

The FTC's 2024 rule banning fake reviews and testimonials signals that disclosure and authenticity expectations are hardening — not softening.

Trend 3: A Generational Divide That Cuts Both Ways

Nielsen's 2021 study identifies Millennials and Gen X as the generations most trusting of advertising globally. Credos provides more precise UK figures:

- 50% of young people trust the ads they see or hear

- Just 22% of those over 55 trust advertising

- Younger generations are nearly four times more likely to trust online advertising than older consumers

That last figure surprises people who assume younger audiences are the most skeptical. It reflects where they spend their time: in digital environments where advertising is expected and familiar, not intrusive. Older consumers' distrust runs deeper, shaped by decades of broadcast overexposure and less familiarity with digital formats.

Trust assumptions, in other words, can't be applied uniformly across age bands. A 30-year-old and a 65-year-old have fundamentally different relationships with the same ad format.

Trend 4: Traditional and Editorial Channels Holding Ground

TV advertising continues to outperform most digital formats in consumer trust. The numbers tell a clear story:

| Format | Trust Level |

|---|---|

| TV ads (US) | 68% |

| Newspaper ads (US) | 67% |

| Magazine ads (US) | 67% |

| TV ads (UK) | 41% |

What connects these channels is perceived legitimacy. Brands that advertise in regulated, editorially governed environments inherit some of that credibility — a dynamic that holds whether the medium is broadcast or print.

Which Ad Channels Consumers Trust Most

Nielsen's most complete public global channel ranking comes from its 2015 study of 30,000 respondents across 60 countries. While older than the 2021 study, it remains the most comprehensive publicly available table:

| Rank | Format | Global Trust |

|---|---|---|

| 1 | Recommendations from people I know | 83% |

| 2 | Branded websites | 70% |

| 3 | Consumer opinions posted online | 66% |

| 4 | Editorial content (newspaper articles) | 66% |

| 5 | TV ads | 63% |

| 6 | Brand sponsorships | 61% |

| 7 | Newspaper ads | 60% |

| 8 | Emails I signed up for | 56% |

| 9 | Online video ads | 48% |

| 10 | Ads on social networks | 46% |

| 11 | Mobile ads | 43% |

| 12 | Online banner ads | 42% |

| 13 | Text ads on mobile | 36% |

The table captures established formats, but two emerging channels are shifting how planners think about recall and influence.

Emerging Formats Worth Watching

Podcast advertising punches above its weight on recall. Nielsen's 2023 emerging media research reports 71% aided recall for podcast advertising, with host-read formats performing even stronger — a figure that matches or exceeds television recall benchmarks.

Streaming integrations are building purchase influence. Nielsen data shows 52% of consumers aged 35-49 and 49% of those aged 18-34 are influenced to purchase products they see integrated into streaming content — making branded integration a high-trust format in an environment where pre-roll ads are increasingly skipped.

Back in the ranked table, opted-in email holds a position that's easy to underestimate at 56% — until you consider what that trust is built on.

Why Opted-In Email Occupies a Trusted Middle Tier

The 56% global trust figure for opted-in email reflects something behaviorally important: a subscriber has explicitly invited a brand's communication into their inbox. The advertising context is one of high intent and low clutter.

This is the environment House of Summary's newsletter placements operate within. Across four newsletters — Presidential Summary, Geopolitical Summary, Dubai Summary, and London Summary — the network reaches 500,000+ subscribers, with 254,866+ emails opened daily. Readers have actively subscribed; ads arrive within editorial content they chose to receive. There's no algorithmic interference, no ad blockers, no visual noise competing for attention.

For advertisers targeting executives and decision-makers in the US, UAE, and UK, that's a materially different trust context than programmatic display.

What's Driving the Global Trust Shift

Consumer trust in advertising has been eroding steadily — and three interconnected forces explain why:

Ad saturation and format fatigue. Credos research cites estimates that commercial message exposure rose from around 300 messages per week in 1980 to more than 3,000 per week in recent years. The consequence isn't just irritation — it's behavioral adaptation. Consumers have trained themselves to filter out advertising, producing what researchers call banner blindness and reflexive ad avoidance.

Data privacy anxiety. IAB's consumer privacy research finds 85% of consumers say it's important to be able to see or delete their data, or choose the types and levels of tracking applied to them. Behavioral targeting — the core mechanism of digital advertising — is exactly what consumers distrust most. GDPR in Europe and CCPA in California formalized this concern into regulatory infrastructure, though consumer distrust of data practices was building long before either law passed.

Declining media credibility. In markets where institutional and media trust has eroded, advertising carried by those channels absorbs some of the damage. The Reuters Institute's 2025 Digital News Report documents continuing declines in news media engagement and trust in key markets.

The flip side: IAB research found 84% of consumers say advertising within trusted news environments increases or maintains brand trust — a halo effect that makes editorial context one of advertising's most underused assets.

Future Signals to Watch

AI-Generated Advertising and the Authenticity Problem

Consumer detection of AI-generated ads is accelerating. The IAB reports that 71% of Gen Z and Millennial consumers believe they've seen an AI-created ad, up from 54% the previous year. Among marketers:

- 37% fear audiences will distrust AI-made ads

- Over 60% support mandatory labeling

- Over 70% encountered an AI-related incident in 2025

- 40% had to pause or pull campaigns as a result

For brands that have built equity on authentic storytelling, the proliferation of AI creative represents a trust liability, not a creative shortcut.

Permission-Based and Community-Driven Advertising

That erosion of trust in interruptive formats is pushing budgets toward consent-based channels. Ad blocker growth, cookie strategy uncertainty, and consumer demand for relevance are together accelerating a structural shift toward first-party, opt-in advertising. Newsletters, branded communities, and direct subscriber relationships are positioned as the high-trust formats of the next few years. They require explicit consent and deliver in low-competition editorial environments — two conditions that interruptive digital advertising rarely meets.

Regulatory Pressure on Advertising Claims

The shift toward accountability isn't just consumer-driven. Regulators are stepping up scrutiny across major markets: the FTC's 2024 rule banning fake reviews, the ASA's active influencer disclosure enforcement, and evolving ICO guidance on behavioral targeting consent all point in the same direction. Advertising accountability is tightening.

There's a trust benefit to that visibility. Credos research found that people aware of advertising regulators are twice as likely to trust advertising overall — suggesting regulatory infrastructure, when visible, functions as a trust signal in its own right.

Frequently Asked Questions

What is trust in advertising?

Trust in advertising refers to the degree to which consumers believe an ad is honest, credible, and from a legitimate source. It varies significantly by channel, region, and age group — ranging from very high trust in word-of-mouth recommendations to low trust in mobile and banner formats.

How can brands build trust in advertising?

Focus on enjoyment and relevance over volume, choose channels where audiences have actively opted in, respect data privacy expectations, and build consistent brand messaging over time. Credos research identifies ad overexposure as a leading driver of distrust.

Which advertising channels do consumers trust the most?

Word-of-mouth, branded websites, editorial content, TV advertising, and opted-in email consistently rank highest in global trust studies. Banner ads, mobile ads, and SMS formats rank at the bottom.

Why is trust in advertising declining in some markets?

Ad overexposure, data privacy concerns, misleading claims, and rising ad blocker adoption are the primary drivers. This decline is most pronounced in North America and Europe, where distrust is sharpest and regulatory pressure is highest.

How does trust in advertising vary by region?

Nielsen's 2021 global study confirms that consumers in Latin America, the Middle East, Africa, and Asia-Pacific report notably higher trust in advertising than those in North America and Europe, where skepticism is most pronounced.

Does advertising trust differ by generation?

Millennials and Gen X trust advertising more than Gen Z and those over 55. Younger consumers show stronger trust in digital formats specifically, and are nearly four times more likely to trust online advertising than over-55s, per Credos 2024 research.