Introduction

Credit card advertising covers the full spectrum of paid, owned, and earned channels — from programmatic display and influencer partnerships to email sponsorships and direct mail. In 2025, the field is being reshaped by three converging forces: AI-driven personalization, a fragmented data privacy landscape, and a generation of younger consumers who discovered financial products on TikTok before they ever set foot in a bank.

The stakes are high. With hundreds of millions of active credit cards in circulation in the US alone, competition for new cardholders — and for top-of-wallet status among existing ones — has never been more intense.

Card issuers who identify and act on emerging channel trends early tend to see measurable gains in acquisition efficiency, activation, and retention. The gap between early movers and late adopters is widening fast.

This article breaks down the five major trends defining credit card advertising in 2025 — including why newsletter placements are quietly outperforming several traditional digital channels — what's driving each shift, and where the landscape is heading next.

Key Takeaways

- AI enables individually tailored credit card offers at scale, replacing mass-market campaigns

- Third-party cookie restrictions are pushing advertisers toward first-party data and owned channels

- TikTok, Instagram, and YouTube have become primary discovery channels for younger card segments

- Newsletter and inbox advertising delivers high-attention, algorithm-free placements that bypass ad blockers entirely

- CFPB enforcement of Regulation Z is reshaping creative workflows across every channel

AI-Powered Personalization and Dynamic Creative Optimization

From Demographics to Behavioral Prediction

Generic credit card ads — "earn 2% cash back on everything!" served to anyone with a pulse — are giving way to something far more precise. AI now allows card advertisers to move beyond demographic segments toward behavioral prediction: using transaction signals, browsing patterns, and real-time intent data to match each prospect with the right card offer at the right moment.

A traveler who searched for flights last week might see a targeted pitch for a travel rewards card. A consumer whose spending skews heavily toward groceries gets a cashback card offer instead. Until recently, the execution required enterprise-scale infrastructure that most mid-sized card programs couldn't access.

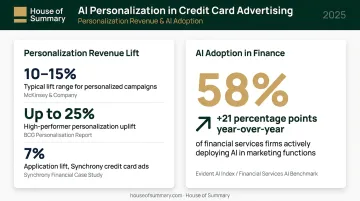

That's changing fast. According to McKinsey, personalization typically drives 10–15% revenue lift across sectors, with some seeing up to 25%. At the card-product level, Synchrony achieved a 7% lift in credit card applications through personalization and A/B testing — which translates to millions in incremental revenue at the volumes card issuers operate.

Dynamic Creative Optimization in Practice

Behavioral targeting identifies who to reach — dynamic creative optimization (DCO) determines what to show them. Rather than producing dozens of ad variants manually, DCO systems assemble ads in real time, mixing the following elements based on what's most likely to convert for each segment:

- Headlines and value propositions matched to spending behavior

- Reward structures (cashback vs. travel vs. points) aligned to transaction history

- APR messaging calibrated to creditworthiness signals

- Visuals and CTAs adapted to placement context

The approach has a track record. JPMorgan Chase's early AI copywriting pilot with Persado produced dramatic CTR improvements. That 2019 result reads as proof-of-concept rather than a 2025 benchmark — but the broader adoption numbers tell the current story: Gartner reported that 58% of finance functions used AI in 2024, up 21 percentage points year over year.

Pre-Qualification Targeting and Compliance Requirements

Pre-qualification targeting is another area where AI is adding value. Card issuers can now deliver pre-approval messaging specifically to consumers who are likely to meet their credit criteria — reducing friction and improving acquisition economics by filtering out audiences who won't qualify.

That efficiency gain comes with a non-negotiable constraint. AI-generated ad copy must still satisfy Regulation Z's "clearly and conspicuously" standard — any automated creative mentioning specific credit terms requires the same disclosures as human-written copy. Compliance review can't be removed from AI workflows. It has to be built into them.

First-Party Data Strategies as the Cookie Era Evolves

A Fragmented Landscape, Not a Clean Break

The "death of third-party cookies" narrative requires some nuance. Google reversed course in 2025 and kept third-party cookies in Chrome, leaving users to manage choices through privacy settings. Safari and Firefox are a different story — WebKit's Intelligent Tracking Prevention blocks third-party cookies by default, and Firefox has rolled out Total Cookie Protection globally.

The practical result: card advertisers can't rely on consistent third-party cookie availability across browsers. Nearly 9 in 10 ad buyers shifted their personalization tactics, ad spend, or data mix in response to these changes, according to IAB's 2024 State of Data report. The trend toward first-party data is clear, even without a universal cookie ban.

Building First-Party Infrastructure

The response from card issuers has been to invest in consent-based first-party data collection. Common collection methods include:

- Email list building and newsletter sign-ups

- Loyalty program enrollment

- App registrations and in-app behavior tracking

- CRM enrichment from existing customer interactions

The goal is audience profiles that power both direct targeting and lookalike modeling — without depending on third-party identifiers.

Chase is the most prominent example of this approach taken to its logical conclusion: Chase Media Solutions uses the company's own transaction data from its 80 million customers to target advertising campaigns — an owned data asset that no privacy shift can diminish.

Co-branded card partnerships offer the same cookie-independent targeting capability for issuers who don't have Chase's scale. When a card issuer partners with an airline or grocery chain, they gain access to purchase-level data that enables relevant targeting without any third-party identifiers. Retail media networks are formalizing this model across the industry.

Social Media, Influencer Marketing, and Gen Z Card Acquisition

Where Younger Consumers Discover Cards

Gen Z turns to social media to research financial products the same way older generations turned to comparison websites. Bread Financial's 2025 research found that social media was the top channel through which Gen Z became aware of the last retailer credit card they applied for. TikTok, Instagram, and YouTube are functioning as the new comparison-shopping environment for this segment.

TransUnion data adds useful context: 84% of credit-active Gen Z consumers held at least one bankcard as of Q4 2023, so they're already in the market and making card decisions based on what they see online.

The Rise of the Finfluencer

Card brands are responding by working with personal finance creators ("finfluencers") and lifestyle influencers who demonstrate card benefits in a format their audiences actually trust. A travel creator showing their airport lounge experience, redeemed on points, carries more weight than a banner ad because the audience already trusts the creator's judgment on how to spend.

The approach requires careful execution:

- Show real redemptions (travel upgrades, cashback use cases) rather than scripted product pitches

- Match creator to product — audiences spot forced financial content fast, and a mismatched partnership hurts both parties

- Disclose every time — FTC guidelines require clear disclosure of material connections between creators and sponsors

Disclosure requirements don't stop at FTC rules. If an influencer post mentions a specific APR, annual fee, or payment amount, it may constitute an advertisement under Regulation Z — triggering full disclosure requirements. Card brands must brief creators on what they can and can't say, and review content before it goes live.

Direct Inbox and Newsletter Advertising

Why Inbox Is Getting a Second Look

Display advertising costs have risen while performance has stagnated. Ad-blocking adoption continues to grow — and it skews toward exactly the audience credit card advertisers want most. GWI data shows affluent consumers are 14% more likely than average to block ads regularly — meaning a high-income executive is more likely to have an ad blocker running than a general internet user.

Newsletter and email advertising sidesteps this entirely. When advertising arrives inside a subscribed newsletter, ad blockers don't apply — the content is delivered directly to the inbox as part of what the reader requested. There's no technical mechanism that strips it out.

The Attention Advantage

The engagement context is also fundamentally different. A reader working through a newsletter moves linearly, without the infinite scroll competing for their attention. That's a different environment than a social feed where an ad has roughly two seconds before the user swipes past.

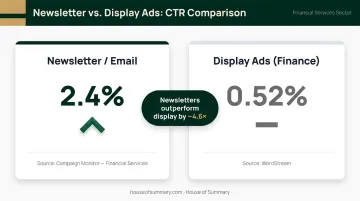

Email benchmarks reflect this. Campaign Monitor's financial services data shows a 2.4% average CTR for financial services emails, compared to a 0.52% CTR for finance and insurance display ads on Google's network per WordStream benchmarks. For credit card advertisers, the match depends on who a newsletter reaches. House of Summary's network, covering global news, geopolitics, and business across Presidential Summary, Geopolitical Summary, London Summary, and Dubai Summary, delivers to over 500,000 subscribers with more than 254,000 emails opened daily.

The audience profile is a natural fit for premium card products, travel rewards cards, and business charge cards:

- C-suite executives, founders, and senior professionals

- High-net-worth individuals across the US, UK, and UAE

- Readers engaged with global business and geopolitical content

That reach translates to measurable results. A Dubai Summary placement delivered click-through rates 4x higher than Google AdWords — a result reported directly by BSH Hausgeräte's CEO. For card brands targeting the upper end of the market, that kind of pre-qualified attention is difficult to replicate through display channels.

What's Driving These Credit Card Advertising Trends

Four forces are accelerating the move toward personalized, compliance-aware, multi-channel credit card advertising:

Technology Acceleration

Machine learning, real-time bidding infrastructure, and modern CRM platforms have made personalized multi-channel campaigns accessible to mid-sized card programs, not just the largest issuers. AI adoption in finance functions jumped 21 percentage points in a single year.

Evolving Consumer Expectations

Millennials and Gen Z expect advertising to reflect their actual spending patterns and lifestyle goals. Mass-market creative is increasingly ignored or blocked — personalization isn't a nice-to-have, it's a baseline expectation.

Regulatory Pressure

CFPB enforcement of Regulation Z has intensified. Trigger terms — any specific credit terms mentioned in an ad, such as APR, annual fee, or minimum payment — require clear and conspicuous disclosure of associated costs. Recent enforcement actions include an $89M order against Apple and Goldman Sachs for misleading Apple Card claims, and a separate action against Bank of America over deceptive rewards sign-up bonus advertising.

AI copy, influencer posts, CTV placements, and email ads all fall within this framework.

Competitive Saturation

With hundreds of millions of cards in circulation, issuers are fighting for both new customers and top-of-wallet status among existing cardholders. That pressure makes every incremental targeting improvement worth pursuing.

Future Signals for Credit Card Advertising in 2025 and Beyond

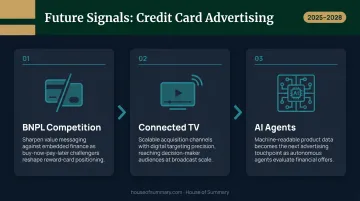

Three developments deserve attention over the next one to three years:

BNPL competition sharpening value messaging. Buy-now-pay-later and embedded finance products are competing directly with revolving credit. Card ads will increasingly need to make an explicit case for why a card beats alternative payment options — which means clearer benefit storytelling and tighter audience targeting.

Connected TV as a scalable acquisition channel. CTV offers card advertisers the reach of broadcast with the targeting precision of digital. Capital One and American Express are already running active streaming creative. As measurement improves, expect more card acquisition budget to shift toward CTV.

AI agents as new advertising touchpoints. Visa's Intelligent Commerce initiative is building infrastructure for AI agents to make purchases on consumers' behalf. If an AI agent is evaluating payment options, the advertising touchpoint isn't a banner or a newsletter — it's whatever information the agent retrieves. Card brands who invest in structured, machine-readable product data now will be better positioned when this model matures.

What separates adaptable card advertisers from reactive ones is ownership. Brands that build first-party data assets and direct audience relationships aren't dependent on platform policy changes or third-party targeting windows closing. Each of these three shifts rewards that same underlying posture.

Frequently Asked Questions

What are trigger terms in credit card advertising?

Trigger terms are specific credit terms (APR, annual fee, minimum payment, finance charge) that, when mentioned in an ad, legally require the advertiser to also disclose the full set of associated costs. For credit cards (open-end credit), this is governed by Regulation Z §1026.16, enforced by the CFPB.

What channels are most effective for credit card advertising in 2025?

Personalized digital channels (paid social, programmatic), influencer partnerships, email and newsletter placements, and direct mail typically deliver the strongest acquisition results. The right mix depends on the target segment — premium card products, for instance, perform well in high-attention formats like newsletters and CTV.

How is AI changing credit card advertising strategies?

AI enables dynamic creative personalization, predictive audience targeting, and real-time offer optimization to match specific card benefits to the right prospect at the right moment. It also powers pre-qualification targeting, improving acquisition economics by filtering for consumers likely to be approved.

How do credit card advertisers target Gen Z consumers?

Gen Z card marketing runs heavily on TikTok, Instagram, and YouTube through collaborations with trusted financial creators. Messaging focused on rewards experiences and financial empowerment consistently outperforms traditional credit feature advertising with this audience.

What regulations apply to credit card advertising in the US?

Credit card advertising is primarily governed by Regulation Z (Truth in Lending Act), enforced by the CFPB. Any specific credit terms stated in an ad must be accurate and available, and trigger terms must be accompanied by full cost disclosures presented clearly and conspicuously.

How do credit card companies measure advertising effectiveness?

Core metrics include customer acquisition cost (CAC), application and approval rates, activation rate, customer lifetime value (CLV), and return on marketing investment (ROMI). Attribution modeling helps assess how each channel contributes across the acquisition funnel.