Introduction

Banking customers no longer wait for a branch visit to make financial decisions. They compare mortgage rates on their phones at midnight, read credit union reviews before ever stepping inside, and switch providers based on a digital experience — or the lack of one. Meanwhile, many institutions are still running marketing strategies built for a branch-centric world, leaving younger and higher-value customers to fintechs and online-only banks that meet them where they already are.

This guide covers the foundational digital marketing channels — SEO, content, email, social media, and paid advertising — plus the modern disruptions reshaping them, particularly AI search. Each channel connects back to the same goal: building trust at every stage of the customer relationship, from the first search query to long-term retention.

Key Takeaways

- Financial institutions that don't invest in digital marketing are already losing ground to fintechs that do

- SEO, content, email, social, and paid ads each serve a distinct purpose and perform best together

- Follow the 80/20 rule: 80% of your content should educate and add value, not pitch products

- AI search is intercepting organic traffic — optimize for how AI surfaces answers, not just how Google ranks pages

SEO and Website Optimization: Getting Found When It Matters Most

A bank's website is its primary branch. Unlike a physical location, it needs to perform at 2 a.m. on a mobile device while a prospect compares refinancing options. If it's slow, confusing, or thin on useful tools, that prospect is gone.

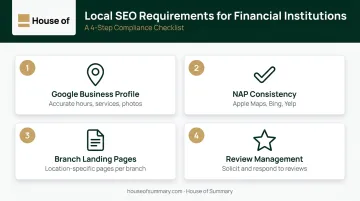

Local SEO Is Where Banks Win

For community banks and credit unions especially, local search is one of the most direct paths to high-intent prospects. Someone searching "credit union near me" or "best mortgage lender in [city]" is close to a decision. Capturing that search requires:

- A fully optimized Google Business Profile with accurate hours, services, and photos

- Consistent NAP (name, address, phone) information across Apple Maps, Bing Places, and Yelp

- Location-specific landing pages for each branch, not a generic "find a location" page

- Local reviews actively solicited and responded to

These aren't complicated tactics, but most institutions are inconsistent with them — which makes consistency a genuine competitive edge.

On-Page SEO That Compounds Over Time

Product pages and educational content both need proper SEO structure. That means:

- Keyword research targeting product-level queries ("CD rates," "auto loan refinance") and question-based searches ("how to refinance a car loan," "what credit score do I need for a mortgage")

- Clear header hierarchy (H1 for page topic, H2s for major sections) that helps search engines understand page structure

- Internal linking between product pages and related blog content — a mortgage rates page should link to your "how mortgage rates work" article

- Image alt text and proper meta descriptions on every page

Individually, none of these moves the needle overnight. Consistently applied, they build into real organic visibility over six to twelve months.

Technical Performance Directly Affects Conversion

Site speed isn't just a technical concern — it's a revenue concern. Research from Deloitte and Google found that a 0.1-second mobile speed improvement was associated with a 10% increase in conversion rate for financial services sites, along with 8% more pages per session.

The cost stakes make this concrete. WordStream's 2026 benchmarks put the average cost-per-click in Finance & Insurance paid search at $3.39, with a cost-per-lead of $74.44. Sending paid traffic to a slow, poorly designed site burns that budget without return. Every dollar earned through SEO reduces that dependency on paid channels.

On-page engagement tools close that loop. Loan calculators, rate comparisons, and account finders give visitors a concrete reason to stay and a natural path toward conversion. They also earn backlinks and social shares without requiring active promotion.

Content Marketing: Building Trust Before the First Transaction

Financial decisions are high-stakes. Nobody opens a mortgage or moves their retirement savings based on a banner ad they saw once. The trust that precedes those decisions gets built over time, through repeated exposure to useful, honest information. Content marketing is how institutions build that trust at scale.

The 80/20 Rule in Practice

The principle is straightforward: roughly 80% of your content should be genuinely educational and non-promotional. The remaining 20% can reference your products — but only in service of answering the customer's actual question.

What does 80% educational look like?

- Budgeting guides and debt payoff calculators

- Mortgage explainers written for first-time buyers, not bankers

- Retirement planning articles that address real anxiety ("am I saving enough?")

- Business cash flow advice for small business owners

- CD and savings rate comparisons that help customers understand their options

PNC's Insights hub — covering Personal Finance, Small Business, and Wealth Management — is a working example of this approach. The pages lead with customer questions, not product features. Regions Bank's segmented Insights Library (Personal, Small Business, Commercial, Wealth) demonstrates a related principle: the navigation itself signals that the institution understands it serves different audiences with different needs.

Segment Your Content by Audience

A community bank serving personal banking customers, small business owners, and wealth management clients needs differentiated content for each group. What matters to a first-time homebuyer is entirely different from what concerns a business owner managing payroll.

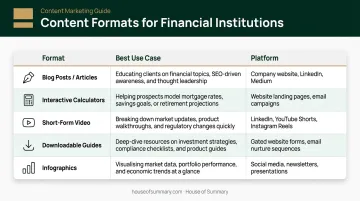

Content formats by stage and platform:

| Format | Best Use Case | Platform |

|---|---|---|

| Blog posts / articles | SEO, trust-building, educational | Website |

| Interactive calculators | High-stakes decisions (mortgage, CD, loan) | Website |

| Short-form video | Financial literacy, product awareness | Instagram, LinkedIn |

| Downloadable guides | Lead generation, deeper engagement | Website, email |

| Infographics | Complex concepts made visual | Social, email |

Supplementing Original Content

Creating high-quality financial content consistently is time-consuming and costly to sustain alone. Licensed or curated content from credible sources keeps publishing frequency consistent without stretching your team thin.

Done well, it also adds value:

- Third-party data and research lend authority your original content can't self-generate

- Curated explainers fill topic gaps where you lack in-house expertise

- Syndicated content from recognized financial publications reinforces trust with skeptical readers

- A mix of original and licensed pieces reduces the pressure of producing everything from scratch

Email Marketing and Newsletter Advertising: The Inbox Advantage

Email remains the most direct relationship channel available to financial institutions. Unlike social media (algorithm-dependent) or search (increasingly intercepted by AI), email reaches customers on your terms.

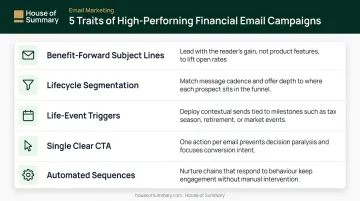

High-Performing Financial Email Campaigns

The basics matter more than most institutions admit. High-performing campaigns share these traits:

- Benefit-forward subject lines that promise specific value ("Your mortgage rate lock expires in 14 days")

- Segmentation by lifecycle stage — prospects, new account holders, long-term customers, and lapsed customers each need different messages

- Life-event triggers — a customer who recently made a large deposit, inquired about a mortgage, or registered a business is signaling intent; your emails should reflect that

- Single, clear call to action per email — not three competing links

- Automated sequences for new account onboarding, loan application follow-ups, and annual financial review invitations

Mailchimp's December 2023 benchmarks put the average click-through rate for Business & Finance emails at 2.73% — compared to display ad CTR in the same category running around 0.52% based on WordStream benchmarks. Email isn't declining; for financial services, it's outperforming most alternatives.

Newsletter Advertising as a Paid Distribution Channel

Beyond your owned email program, newsletter advertising lets financial brands reach new audiences through established publications that already have their trust. The inbox is clutter-free by design — ads aren't blocked, suppressed by algorithms, or buried under competing visuals.

House of Summary's newsletter network, for instance, offers direct access to over 500,000 subscribers with 254,866+ emails opened daily. The audience skews toward executives, C-suite professionals, and high-net-worth individuals in New York, Los Angeles, London, and Dubai. That's precisely the demographic premium financial services brands need to reach — yet rarely can through programmatic or social channels alone.

House of Summary's publications — Presidential Summary, Geopolitical Summary, Dubai Summary, and London Summary — serve readers already consuming serious, substantive content. Placing a financial brand in that context is fundamentally different from interrupting someone mid-scroll on social media.

First-Party Data Is the Long Game

Third-party cookie reliability remains uncertain. Google has signaled it will preserve user cookie choices rather than deprecate them outright, but Deloitte's guidance is clear: marketers should continue building first-party data infrastructure regardless of browser timelines.

For financial institutions, this means:

- Building owned email subscriber lists deliberately, not as an afterthought

- Implementing a Customer Data Platform (CDP) — software that unifies behavioral, transactional, and demographic data from multiple touchpoints into a single customer view

- Using behavioral signals (pages visited, calculators used, emails opened) to trigger timely, relevant outreach rather than relying on broad demographic assumptions

Banks already collect more first-party data than most industries ever could. The challenge is connecting it to marketing systems in compliant, actionable ways.

Social Media and Paid Digital Advertising: Staying Visible at Every Stage

Organic Social vs. Paid — Different Jobs, Same Strategy

Organic social and paid advertising serve different stages of the customer journey. Used together, they reinforce each other rather than compete for budget.

Organic social handles the long game:

- Builds brand personality and community trust

- Establishes financial literacy credibility

- Reflects employee culture and local presence

Paid advertising handles immediate conversion:

- Drives targeted traffic to specific product pages

- Generates measurable leads with trackable ROI

- Retargets high-intent visitors who didn't convert

Paid ads should always drive to purpose-built landing pages, not your homepage. Someone clicking a "refinance your auto loan" ad should land on a page about auto loan refinancing — with a calculator, rate information, and a clear application path. Sending paid traffic to a generic homepage wastes every dollar spent getting the click.

Behavioral Targeting Over Demographics

Targeting "adults aged 25-45" is a poor proxy for intent. Financial institutions with strong digital infrastructure can target based on actual behavior:

- Visitors who reached the mortgage application page but didn't submit

- Customers who used a retirement calculator but haven't opened an IRA

- Prospects searching competitor terms on Google

- Existing customers whose account activity suggests an upcoming major purchase

This level of precision requires connecting your CRM and behavioral data directly to your ad platforms. A CDP makes that connection possible.

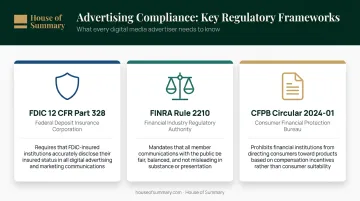

Compliance Is Non-Negotiable

Every digital content type (social posts, paid ads, emails, blog posts) operates within a regulatory framework:

- FDIC (12 CFR Part 328): Governs required signage and accurate representation of insured status in digital advertising

- FINRA Rule 2210: Requires fair, balanced, and non-misleading communications for member firms

- CFPB Circular 2024-01: Warns against digital tools that steer or preference products based on compensation rather than consumer interest

Meeting these requirements consistently comes down to process. Build a pre-approved messaging library. A content calendar with compliance-cleared templates dramatically reduces the time from idea to publication without increasing legal exposure.

The AI Search Shift: What Financial Marketers Need to Do Now

The Traffic Problem Is Already Here

According to SparkToro's 2024 zero-click search study, 58.5% of US Google searches ended without a click (no visit to any website). Meanwhile, Search Engine Land reported that Google AI Overviews appeared on 13.14% of US desktop searches in March 2025, up from 6.49% in January — that's a 102% increase in two months.

Informational queries like "what is a HELOC" or "how do CD rates work" are exactly the content banking SEO teams have relied on for organic traffic. AI is now answering many of these directly. Traffic from those queries is declining, and it won't recover.

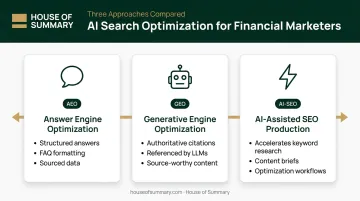

Three Approaches Worth Understanding

Financial marketers don't need to abandon SEO. They need to extend it:

- Answer Engine Optimization (AEO): Structuring content so AI systems can extract and present it as a direct answer through clear definitions, FAQ-style formatting, and concise factual claims with sourced data

- Generative Engine Optimization (GEO): Creating authoritative, well-cited content that large language models reference when generating responses ; being cited in an AI answer is the new version of ranking on page one

- AI-assisted SEO production: Using AI tools to accelerate keyword research, content briefs, and optimization so human writers can focus on depth, accuracy, and expertise

None of these replace foundational SEO. They extend it into a search environment where the goal is visibility inside AI-generated answers, not just blue-link rankings.

What Smart Institutions Are Prioritizing

The institutions best positioned for this shift share a few common characteristics:

- First-party data infrastructure so they're not dependent on platform-mediated reach that changes when algorithms change

- Content treated as authority signal rather than a traffic mechanism — proof that the institution understands the financial topics its customers care about

- Budget reallocation toward activation : acquiring an account that never transacts wastes acquisition spend. Institutions shifting investment toward onboarding, engagement, and cross-sell are seeing better lifetime value from the same customer base

What ties these priorities together is control. Channels dependent on platform algorithms, third-party cookies, or organic search click behavior are less reliable than they were two years ago. Email lists, first-party data, and direct customer relationships are more valuable — and that gap is widening.

Frequently Asked Questions

What is the 70/20/10 rule in digital marketing?

The 70/20/10 framework splits your content mix: 70% goes to proven, audience-relevant educational material, 20% to curated or adapted content from other sources, and 10% to experimental or promotional content. For banks, this means financial education content should dominate your publishing calendar, with product promotion as the exception rather than the rule.

What are the services offered by digital banking?

Digital banking services include online account management, mobile check deposits, bill payment, fund transfers, loan applications, and financial planning tools. Marketing these services effectively requires meeting customers on the platforms where they already research and compare them — primarily search, social, and email.

How do banks use social media for marketing?

Banks use social media to build brand personality, share financial education content, highlight community involvement, and respond to customer questions. Platform choice matters: LinkedIn for B2B audiences, Instagram for lifestyle content, Facebook for community engagement. Consistent posting and prompt responses to comments and reviews are what separate effective programs from forgettable ones.

What makes digital marketing for financial institutions different?

Financial marketing carries regulatory compliance requirements, extended decision timelines, and a higher trust burden than most consumer categories. Prospects research financial products for weeks or months before acting, which means educational content and reputation management are more decisive here than in almost any other sector.

How can small banks and credit unions compete with fintechs online?

Community banks and credit unions have genuine advantages fintechs can't replicate: an established local presence and real community relationships built over years. Prioritize local SEO, produce educational content that reflects your community's specific financial concerns, and prioritize member experience at every digital touchpoint. Marketed well, authenticity and local relevance are genuine competitive advantages — ones fintechs have no easy way to manufacture.